Management Team Explanation

Importance of the management team

In small companies, the management team is an absolutely critical factor. However, for an individual investor it is difficult to visit the company and meet with management to get first-hand knowledge of how they run the business and allocate capital.

Moreover, in periods of high market volatility, being invested in a small company can be especially tough, as any management mistake is magnified.

It is very easy to make mistakes when assessing the management team of a small company, and those mistakes can lead to permanent capital loss—one of the biggest risks for any investor.

The success of an investment depends heavily on the quality of the management team:

- In large companies, management quality accounts for about 30–40% of the investment outcome.

- In small companies, this dependence can rise to 70%, which implies significant risk.

Key traits of a good team

A good management team should meet the following criteria:

Proven track record: We look for managers with an impeccable history of value creation at the companies they have been part of—no fraud, accounting manipulation or scandals.

Capital management focused on value creation: Capital allocation should be long-term oriented. We look for deeds, not words, and for stated targets to be met over time.

Reasonable compensation: Salaries and stock options (stock-based pay) should be moderate and properly aligned with company profit. As a rule of thumb, they should not exceed 15–20% of profit, although there are justified exceptions.

Stock-based pay and incentives

One key question is: how do you know if stock-based pay is excessive? The only way is to compare it with incentives at other executives in the sector.

The incentives we care about are those tied to long-term value creation, such as:

- EPS

- FCF per share

- ROIC

Examples

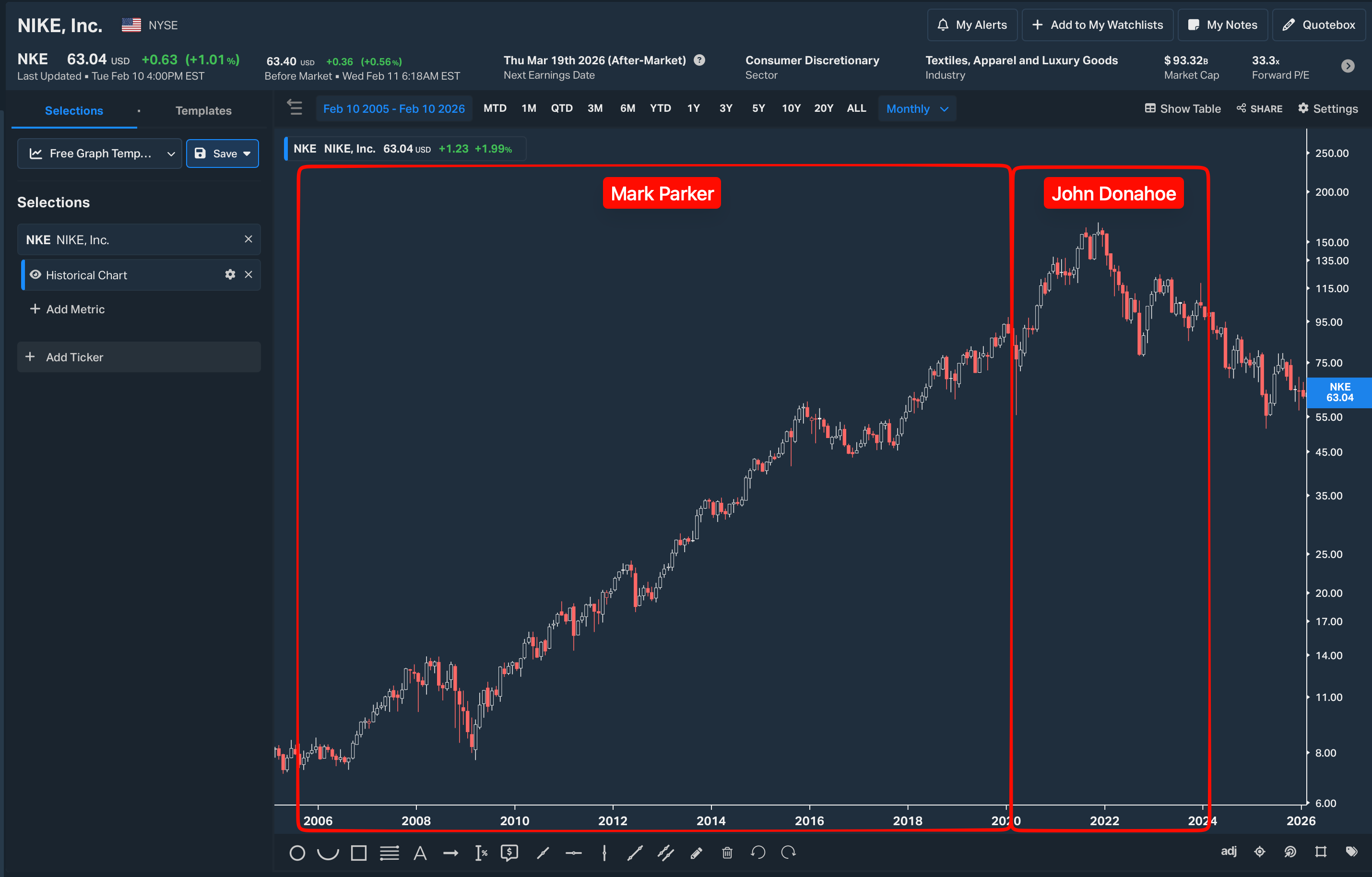

Nike CEO

In early 1977, Nike had a very specific policy.

Nike was considered a strong brand, built over time. Destroyed in just 4 years.

- Well run under Mark Parker 2006–2020

- Poorly run under John Donahoe (ousted): 2020–2024

Starbucks CEO

Howard Schultz 1986–2000, 2008–2017, 2022–2023: The architect of the brand. His vision turned a small coffee roaster in Seattle into the global giant it is today, returning on multiple occasions to rescue the company’s essence in times of crisis.

Laxman Narasimhan 2023–2024 (ousted): Amid a historic labor relations crisis and a growing wave of unionization, Narasimhan made a fatal communication mistake: stating in an interview that his workday strictly ended at 6 p.m. With a compensation package of $14 million—more than 1,000 times the salary of an average barista—his remarks were seen as a total disconnect from the reality of his employees. This lack of empathy and commitment accelerated his abrupt departure after just 18 months in the role.

Exemplary CEO

Jeff Bezos is considered by many to be one of the best CEOs in history, thanks to a rare combination of strategic vision, obsessive execution and operational discipline.

Insiders

Insiders are people directly or indirectly linked to a company:

- Direct link: CEO, CFO, board members, senior executives, etc.

- Indirect link: Close relatives (spouse, children) or other people with access to material information.

All share purchases and sales by insiders must be disclosed publicly and are closely monitored by regulators in each country, to prevent misuse of inside information.

A good way to look up this information is the Insider Screener site: https://www.insiderscreener.com/en/

Interpreting insider transactions

- In any type of company, an insider buying a significant proportion of shares is a green flag that we should not ignore.

- In large companies, where information asymmetry is low or almost nonexistent, these purchases can indicate that the company is trading at an attractive price.

- In mid-sized and especially small companies, information asymmetry is much higher. In these cases, besides signaling possible undervaluation, insider purchases can reflect that they are using their better knowledge of the business.

Fraud and misconduct in companies

“Financial shenanigans” or accounting shenanigans are actions designed to mask or misrepresent a company’s true financial performance or real situation.

These practices can range from relatively minor breaches based on creative interpretations of accounting standards to serious accounting fraud sustained over years.

In most cases, when it emerges that a company’s supposedly excellent financial performance was due to accounting shenanigans rather than good management, the impact on the share price is usually devastating, affecting both the stock price and the business’s future prospects.

Depending on severity, the consequences can range from a sharp fall in the stock to bankruptcy and dissolution of the company.

Types of companies where fraud is more likely

Fraud is more common in:

- Companies under pressure to maintain high earnings or revenue growth rates in order to support high multiples and keep raising capital.

- Companies that promise overly optimistic projections (SPACs, IPOs).

- Companies that need constant capital injections to survive (loss-making companies).

- Executives with a large part of their compensation tied to stock-based pay whose value depends on the share price.

- Small and mid caps, where oversight is lower.

- “Overheated” IPOs that sell stories that are too good to be true (very typical with SPACs).

- Heavily regulated companies.

- Companies that make many acquisitions (risk of value destruction and hiding organic sales).

- Real estate and construction companies, historically prone to conflicts of interest.

Red flags guide

Is it easy to spot fraud or accounting shenanigans? No. It is very difficult or even impossible.

We will group the warning signs into three levels:

Environment and reputation

Exposure to short sellers: Companies on the radar of research firms (such as Gotham City or Muddy Waters). A short report can tank the share price on legitimacy concerns.

- gothamcityresearch.com

- muddywatersresearch.com

- kerrisdalecap.com

- wolfpackresearch.com

- qcmfunds.com

Promotional narrative: Be wary of executives who focus more on “selling” the stock than on explaining the business.

Circle of competence: If you do not fully understand the business model, the risk is not the company but your lack of control over the investment.

Accounting quality and audit

Data integrity: Check the auditor’s reputation and any sudden changes of audit firm.

Collection gap: If sales grow but Working Capital spikes, the company may be inflating revenue it is not collecting.

Financial engineering: Overuse of “adjusted” metrics (adjusted EBITDA) and repeated use of one-off items to hide operating expenses.

Governance and insiders

Leadership stability: Unusual turnover of CEOs or CFOs is often the prelude to a “balance sheet cleanup” or the discovery of irregularities.

Alignment of interests: Analyze management (insider) transactions, their salaries and whether their stock option plan harms shareholders.

Integrity track record: Look into any history of fraud or prior scandals involving management. Past ethics often predict future behavior.